Heavy industry components, such as lines, pipes, silos, turbines, and cranes and automotive components, such as bunkers, are prone to abrasion and corrosion. The interruption caused by the breakdown of a single component leads to major expenditures to plant owners. In order to prevent such incidents in the workplace, the installation of wear protection systems for heavy duty machinery is vital. The global heavy duty wear protection systems market is expected to expand at a CAGR of 4.3% from 2015 to 2024 owing to expenditures incurred by plant owners for replacement, efficiency improvements, and environmental legislations.

With rapid industrialization and urbanization around the globe, a notable rise in the growth of heavy industries such as oil and gas, iron and steel, and construction and mining has been witnessed over the past few years. Due to rising industrialization, wide-scale deployment of machinery and automotive parts is recorded, which in turn has created a beneficial prospect for the growth of the heavy duty wear protection systems market. The early-life failure of wear components, causing loss of production time, has further pushed end-users to install the latest wear protection systems for machinery. Increasing end-use market applications of the wear protection systems and further innovation in terms of design are also opportunities to supplement the growth rate. However, the growing market for wear-proof components and fluctuating heavy industry project costs are hampering the growth of the heavy duty wear protection systems market.

Planning to lay down future strategy? Perfect your plan with our report brochure here https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=8335

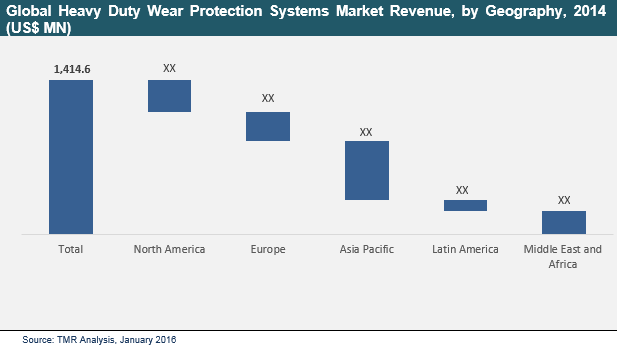

The heavy duty wear protection systems market is segmented on the basis of material type, end-use industry, and geography. Segments on the basis of material type are ceramic, rubber, steel, and plastic. Rubber wear protection systems can be further segmented on the basis of product type into lining systems and coating systems, of which the coating systems segment is expected to grow the fastest. Reported end-use industries deploying wear protection systems encompass transportation and automotive, oil and gas, iron and steel, mining, power plants, wood, pulp and paper, construction, and others such as planer mills, agriculture and farming, F&B and marine. The oil and gas industry, along with the construction and mining industries, are expected to grow the fastest in terms of their deployment of wear protection systems. The heavy duty wear protection systems market has been studied for five geographies: North America, Europe, Asia Pacific, Latin America and, Middle East and Africa.

The Asia Pacific region recorded the highest implementation of heavy duty wear protection systems over the past few decades and is expected to dominate the wear protection systems market with the highest CAGR over the forecast period. This growth rate is anticipated due to the large-scale installations of heavy industries across major economies such as China, Japan, India, Indonesia, and Australia.

The heavy duty wear protection systems market is fragmented in nature, with many global and local companies present. The key strategies undertaken by most internationally acclaimed players were mergers and acquisitions in order to dominate the global wear protection systems market. Furthermore, several SMEs operating exclusively in the wear protection domain have adopted joint venture strategies and long-term service agreements in order to strengthen their market position.

Looking for exclusive market insights from business experts? Request a Custom Report here https://www.transparencymarketresearch.com/sample/sample.php?flag=B&rep_id=8335

Key players in the heavy duty wear protection systems market include Sandvik Construction (Sandvik Group), Metso Corporation, CeramTec GmbH, FLSmidth & Co. A/S, Kalenborn International GmbH & Co. KG, Bradken Limited, ThyssenKrupp Industrial Solutions AG, Sulzer ltd, and Thejo Engineering Limited.